- Summits

- Sponsorship

- Retreats

- Media Opportunities

- News

- About

Changes in the MedTech industry can happen all of a sudden, but keeping an eye on the right trends can make all the difference. With new innovations, shifting investment landscapes, and evolving regulations, how can industry professionals stay on top? The Zapyrus 2024 MedTech Report by Kevin Saem, Brand Founder of Zapyrus, helps answer that. It offers a deep dive into the key trends, emerging technologies, and updates you need to know to stay ahead in the fast-paced world of medical technology.

Here are the key takeaways from the Zapyrus 2024 MedTech Report, which provides a comprehensive outlook on the MedTech industry heading into 2025.

Zapyrus stresses the importance of going beyond just tracking funding numbers. The report reveals that while MedTech companies secured substantial funding in 2024, this is only the beginning. There’s often a lag between funding and the initiation of clinical trials—sometimes taking 6 to 12 months. The influx of funding in 2024 will fuel a surge in clinical trial activity throughout 2025. Contract Research Organizations (CROs), which help manage these trials, need to be ready to capitalize on this increase in demand.

Another surprising insight from the report is the significant role of smaller companies in driving innovation. In fact, most of the MedTech companies receiving funding (the majority of which are under 200 employees) are smaller, more agile firms. This indicates that service providers such as CROs and Contract Development and Manufacturing Organizations (CDMOs) must tailor their strategies to accommodate the unique needs of these smaller firms, such as regulatory consulting and prototype design.

The Zapyrus report also presents an interesting shift in how clinical trials are being initiated. It highlights that non-funded MedTech companies are initiating twice as many clinical trials as those that have secured funding. This finding challenges traditional methods of identifying opportunities in the MedTech space, which typically rely on tracking funding announcements. These non-funded companies, which are pushing forward with innovation without the backing of venture capital, are operating under the radar and represent hidden gems that service providers should target for collaboration.

On a more concerning note, the report points out that the number of FDA device recalls has been increasing, which could initially seem alarming. However, this rise in recalls is actually indicative of stricter regulations and a heightened focus on device safety, ultimately benefiting patients. While this might seem negative, it presents an opportunity for regulatory consulting firms to assist companies in navigating the complex regulatory landscape, ensuring that their products meet the highest safety standards and avoid costly recalls.

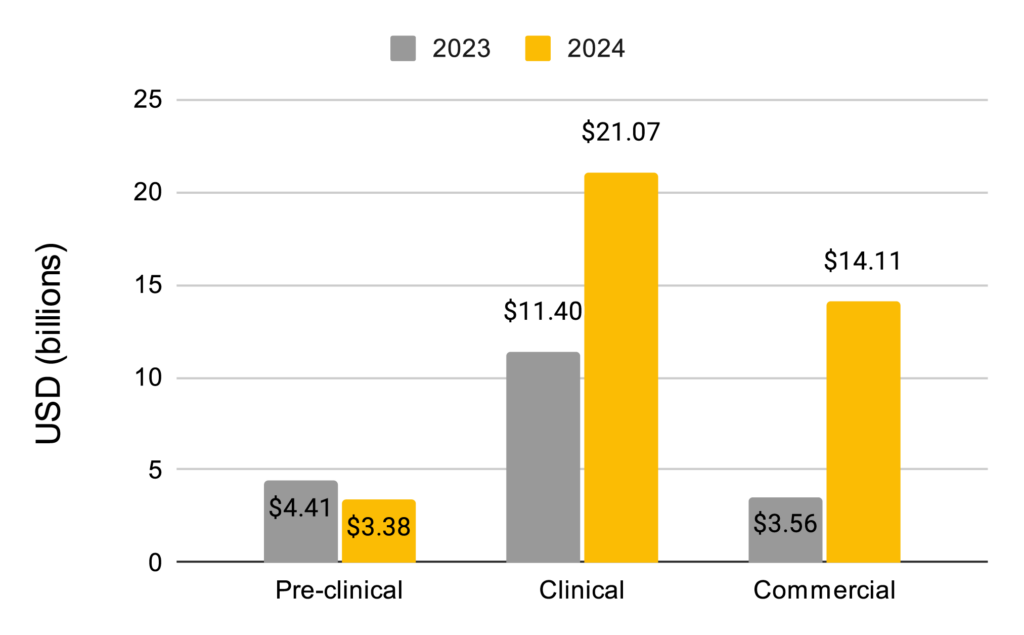

A significant shift is also evident in how funding is being distributed across different stages of company maturity. In 2023, a large portion of funding went to preclinical companies, still in early R&D. However, 2024 saw a drastic shift, with investment in clinical-stage companies almost doubling to $21 billion, indicating that many companies that received funding in 2023 have transitioned to clinical development. This surge presents significant opportunities for service providers specializing in clinical trials.

Additionally, funding for commercial-stage MedTech companies—those with products already approved and on the market—also saw a substantial boost in 2024, with $10.5 billion in funding. These companies will require assistance with scaling operations, marketing, and penetrating new markets, signaling an uptick in demand for services related to commercialization.

The report breaks down the therapeutic areas attracting the most investment. Medical devices received a major boost, with $20 billion more funding in 2024 compared to the previous year, solidifying their dominance in the MedTech sector. However, other areas like in vitro diagnostics (IVD) and Software as a Medical Device (SaMD) received considerably less funding, with IVD receiving $3 billion and SaMD trailing behind with just $900 million. This suggests that service providers looking to tap into well-funded areas should focus on medical devices, which will remain a key area of innovation in 2025.

In terms of therapeutic areas, the biggest funding increases went to high-risk fields such as cardiovascular, neurology, oncology, urology, and gastroenterology, where the stakes are high, and specialized services are crucial. Companies working in these fields are expected to need comprehensive support, from clinical trials to advanced manufacturing, and they will likely pay a premium for such expertise.

A notable highlight from the report is the surge in investment in women’s health technologies, which received its largest amount of funding in the past 20 years. This represents a significant opportunity for service providers with expertise in this area to play a key role in advancing innovations that could improve women’s health on a global scale.

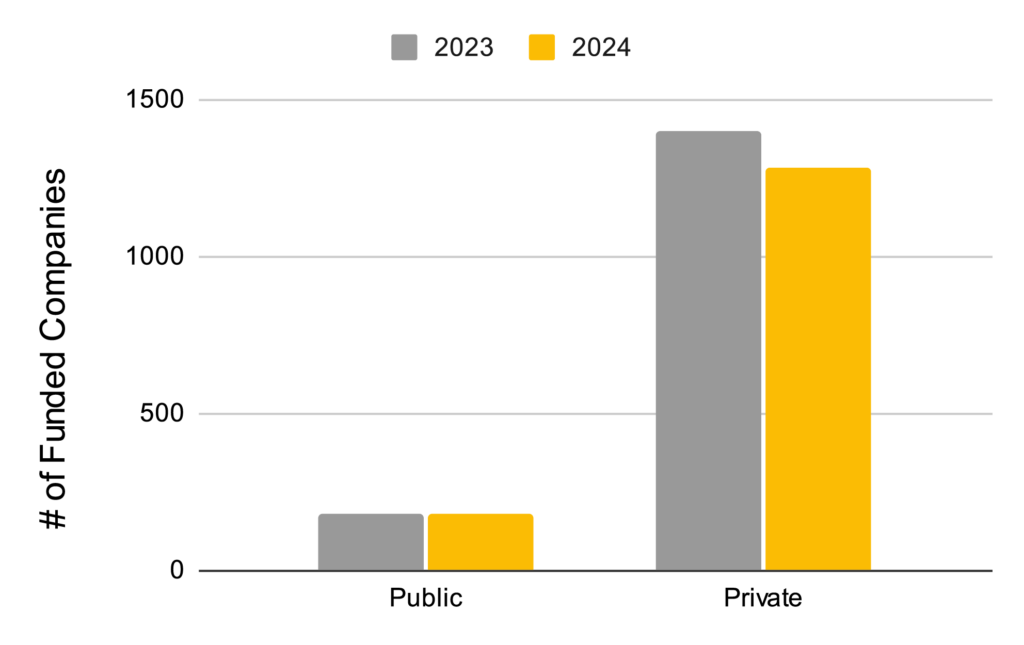

The report also explores the funding dynamics between public and private MedTech companies. Public companies, typically more financially stable, did not see much fluctuation in funding between 2023 and 2024. Service providers targeting public companies need to look beyond funding announcements and focus more on factors like product development timelines, regulatory milestones, and commercialization efforts.

In contrast, private companies saw a decrease in the number of funding rounds but experienced a dramatic rise in the size of individual funding deals. The average deal size for private companies that received funding more than doubled in 2024, indicating a shift towards quality over quantity in investor decisions. Service providers targeting private companies will need to be strategic, understanding each company’s specific stage of development and their unique needs to establish valuable partnerships.

Another important finding in the report relates to FDA device approvals, specifically the decline in 510(k) submissions from 2023 to 2024. The 510(k) process, a pre-market notification for medical devices to demonstrate substantial equivalence to existing devices, saw fewer approvals in 2024. However, only about 10% of 510(k) submissions typically require clinical trials, meaning CROs targeting 510(k) approvals must be strategic and focus on devices that are more likely to need their services, such as complex or high-risk devices.

Despite a decline in the total number of clinical trials initiated in 2024 compared to 2023, high-risk medical devices remain a strong area of focus. Therapeutic areas like cardiovascular, neurology, oncology, orthopedics, urology, and women’s health will continue to be high-priority areas where specialized clinical trial services are in high demand. CROs who can focus on these areas will be well-positioned to secure contracts in the coming years.

The Zapyrus 2024 MedTech Report reveals that while traditional indicators of success—such as funding rounds—remain important, MedTech companies and service providers must now adopt a more data-driven, strategic approach. By focusing on key trends like clinical trial activity, FDA approvals, and sector-specific funding, service providers can better anticipate opportunities and position themselves for success in 2025.